When you pick up a prescription at the pharmacy, you probably don’t think about how much the pharmacy actually gets paid for it. But that payment - called pharmacy reimbursement - is what keeps the doors open. And when a generic drug replaces a brand-name one, the money flow changes in ways that affect pharmacies, patients, and even your out-of-pocket costs.

Generic substitution isn’t just about saving money. It’s a financial engine. In 2023, over 90% of all prescriptions filled in the U.S. were for generic drugs, up from just 33% in 1993. That’s a massive shift. But here’s the catch: even though generics are cheaper to make, how pharmacies get paid for them can make the difference between staying in business or closing down.

How Pharmacies Get Paid for Generics

Pharmacies don’t just charge you what they paid for the pills. They get reimbursed by insurance companies or Pharmacy Benefit Managers (PBMs) - middlemen who manage drug benefits for insurers. The two main ways they’re paid are cost-plus and Maximum Allowable Cost (MAC).

Cost-plus reimbursement means the pharmacy gets its actual cost for the drug plus a fixed fee - say, $4.50 - for dispensing it. Simple, right? But here’s the problem: if the pharmacy buys a generic for $1.20, and gets paid $5.70 total, their profit is $4.50. That’s fine. But if the same drug drops to $0.80 next week, the pharmacy still only makes $4.90. Their profit barely changes, even though their cost fell. That’s not a reward for efficiency - it’s a cap.

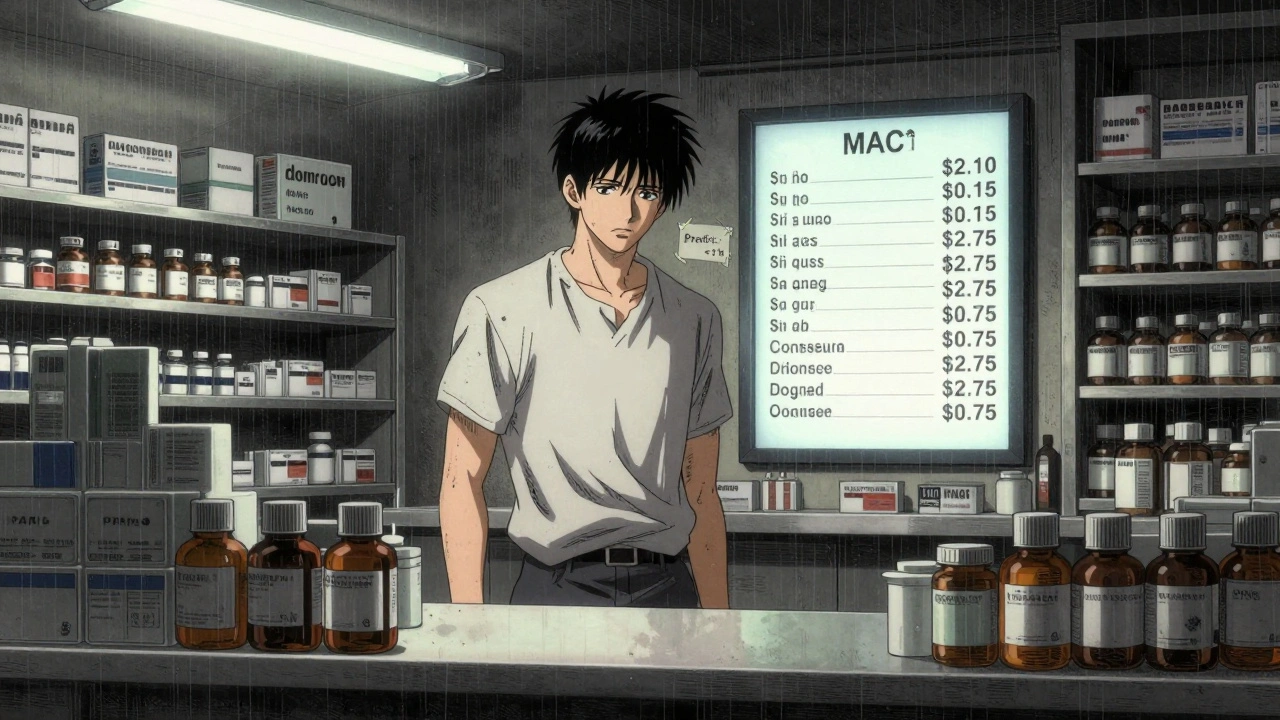

MAC lists are where things get messy. PBMs create these lists that say, “We’ll pay no more than $2.10 for this generic lisinopril.” Sounds fair. But here’s the twist: PBMs often set MAC prices higher than what pharmacies actually pay. Why? Because they pocket the difference. This is called spread pricing. A pharmacy might buy the same lisinopril for $0.90, but the PBM reimburses $2.10. The $1.20 difference goes straight to the PBM - not the pharmacy, not the patient, not the insurer. The pharmacy just gets paid and moves on.

And here’s the kicker: pharmacies have no idea what the real acquisition cost is. They don’t see the invoice from the wholesaler. They just see the reimbursement amount on the screen. So they can’t even negotiate or shop around.

Why Pharmacists Push Generics - Even When It Doesn’t Help

Generics are cheaper to produce. That’s why they’re supposed to save money. But the financial incentive isn’t always aligned with what’s best for the system.

Pharmacies make, on average, 42.7% profit on generics - compared to just 3.5% on brand-name drugs. That’s a huge margin. So pharmacists are naturally going to push generics. But what if there are two generics for the same drug? One costs $0.75. The other costs $2.10. Both work the same. The PBM’s MAC list says $2.10 is the max they’ll pay. So the pharmacy gets paid $2.10 for the $0.75 drug. The PBM pockets $1.35. The pharmacy doesn’t care - they still get paid. The patient pays the same copay. The insurer pays more than they should.

Studies show that in some cases, the price difference between two generic versions of the same drug was over 20 times higher. That’s not a pricing error. That’s a system designed to let PBMs profit from complexity.

And it’s not just about the same drug. PBMs sometimes switch you to a different generic - a different dosage form, or a different manufacturer - that’s more expensive but still considered “therapeutically equivalent.” That’s called therapeutic substitution. It sounds safe. But if the cheaper version exists, why aren’t you getting it?

The Real Winners and Losers

Who wins in this system? PBMs do. The three biggest ones - CVS Caremark, Express Scripts, and OptumRx - control 80% of all prescription claims. They set the rules. They control the MAC lists. They decide which generics get paid more. And they profit from the gap between what they pay pharmacies and what they charge insurers.

Who loses? Pharmacies, especially independents. Between 2018 and 2022, over 3,000 independent pharmacies closed. Why? Because reimbursement rates didn’t keep up with rising rent, labor, and supply costs. Many pharmacies now operate on less than 1% profit after all expenses. That’s not sustainable. Some are forced to stop stocking high-cost specialty drugs - even if a patient needs them - because they can’t afford to lose money on them.

Patients don’t always save money either. Your copay might be $5 for a $2.10 generic - but if the real cost is $0.75, you’re paying more than necessary. And if your plan has a deductible, you’re paying more out of pocket because the drug’s inflated price counts toward your deductible.

What’s Being Done About It?

Regulators are starting to pay attention. The Federal Trade Commission launched investigations in 2023 into PBM spread pricing. They’re asking: Why aren’t MAC lists disclosed to insurers? Why are some generics priced 20 times higher than others with no clinical difference?

The Inflation Reduction Act of 2022 forced Medicare Part D to be more transparent about drug pricing. That’s a start. But commercial plans - which cover most Americans - aren’t covered yet.

Seventeen states now have Prescription Drug Affordability Boards (PDABs). These boards can set “Upper Payment Limits” - basically, a cap on how much insurers can pay for certain drugs. That pushes PBMs to use cheaper generics. But it also risks limiting access if the cap is too low. A cancer drug might be priced at $1,200. If the cap is $800, the pharmacy might not stock it at all. That’s a trade-off.

What’s Next?

Experts predict the system will shift toward value-based reimbursement. That means pharmacies get paid not just for filling prescriptions, but for helping patients stay healthy - like checking adherence, managing side effects, or coordinating care. But that’s still years away.

For now, the system is broken. Generics were meant to save money. Instead, they’ve become a tool for profit extraction. Pharmacies are squeezed. Patients are confused. PBMs are thriving.

The solution isn’t to stop using generics. It’s to fix how they’re paid for. Transparent pricing. Fair reimbursement. Real competition. Without those, the savings from generics will keep disappearing into the gaps between what’s paid, what’s charged, and what’s really spent.

What You Can Do

As a patient, you have more power than you think. Ask your pharmacist: “Is there a cheaper generic version of this?” If they say no, ask if it’s on the MAC list. If they don’t know, ask your insurer. You’re entitled to know what you’re paying for.

If you’re on Medicare or have a large employer plan, look up your plan’s formulary. See what generics are covered and at what tier. Sometimes, switching to a different generic - even if it’s the same drug - can cut your cost in half.

And if you’re a pharmacy owner? Push back. Demand transparency. Join advocacy groups. The system won’t change unless someone pushes.

How does generic substitution affect my pharmacy’s profits?

It depends on how you’re paid. If your reimbursement is cost-plus, your profit doesn’t change much when the drug price drops. If you’re paid through a MAC list, you might make more if the MAC is set higher than what you paid - but you won’t know that number. Most pharmacies make 40%+ profit on generics, but after rent, staff, and overhead, many are left with less than 1% net profit.

Why do some generic drugs cost so much more than others?

Because PBMs set Maximum Allowable Cost (MAC) lists that don’t reflect real market prices. Two generics for the same drug - say, lisinopril - can differ by 20 times in price. The PBM puts the more expensive one on the formulary to increase their spread pricing profit. The pharmacy gets paid the same amount regardless, so they have no incentive to choose the cheaper one.

Can I ask my pharmacist for a cheaper generic?

Yes. Pharmacists are trained to suggest alternatives. If your prescription is for a brand-name drug, ask if there’s a generic. If it’s already generic, ask if there’s a lower-cost version from a different manufacturer. Sometimes switching just one drug saves $50 a month.

Do PBMs always choose the cheapest generic?

No. PBMs often choose generics that maximize their own profit, not your savings. They’re not required to pick the lowest-cost option. Studies show they frequently pick generics priced 20 times higher than alternatives - even when both are equally effective.

Why are so many independent pharmacies closing?

Because reimbursement rates haven’t kept up with costs. Rent, labor, and regulatory compliance have risen, but PBM payments have stagnated or dropped. Many independents now lose money on every generic prescription they fill. Between 2018 and 2022, over 3,000 closed. Chain pharmacies survive because they negotiate better terms - or own the PBMs.

Author

Roger Leiton

December 3, 2025 AT 15:02Bro this is wild 😱 I had no idea PBMs were making bank off generic drug price gaps. My copay’s been $5 for lisinopril for years… but if the real cost is 75 cents? That’s like paying $20 for a $1 coffee. Why am I the one carrying this?

Laura Baur

December 5, 2025 AT 06:08Let us not delude ourselves into believing this is merely a matter of market inefficiency-it is, in fact, a systemic betrayal of the social contract between healthcare providers, insurers, and the vulnerable. The PBM-industrial complex has weaponized pharmacological equivalence to extract rent from the sick, the elderly, and the underinsured. The very notion that therapeutic substitution can be justified while the patient’s out-of-pocket burden remains unchanged reveals a moral vacuum at the heart of American pharmaceutical policy. This is not capitalism-it is predation dressed in white coats and regulatory fine print.

Jack Dao

December 5, 2025 AT 20:56Wow. So pharmacies make 40% profit on generics but still go broke? Lmao. That’s like saying a pizza place makes $10 on each slice but can’t afford the oven. Someone’s lying. Probably the pharmacies. 🤷♂️

dave nevogt

December 6, 2025 AT 08:19It’s heartbreaking when you realize the system was designed to help people-lower drug costs, increase access, streamline care-but instead became a Rube Goldberg machine of middlemen, opaque pricing, and perverse incentives. The pharmacy isn’t the villain here. They’re the last node in a broken chain, trying to keep the lights on while the people above them siphon off the profits. And the worst part? No one’s actually accountable. The PBM doesn’t answer to anyone. The insurer doesn’t know what’s happening. The patient just pays and assumes it’s fair. We’ve outsourced ethics to spreadsheets.

Arun kumar

December 7, 2025 AT 14:12India also have this problem but in reverse. We have cheap generics but pharmacists push expensive ones because they get kickbacks. Same game, different country. The system is rigged everywhere. 😔

Steve World Shopping

December 8, 2025 AT 03:26The structural asymmetry inherent in the PBM-value chain is a textbook example of information asymmetry exploited at scale. The MAC list functions as a non-transparent pricing mechanism that obfuscates true marginal cost, enabling rent-seeking behavior by vertically integrated entities. The lack of bidirectional price visibility creates a monopsonistic environment wherein pharmacists are price-takers, not participants. This is not a market-it is a controlled extraction regime.

Rebecca M.

December 8, 2025 AT 18:13So let me get this straight… I’m paying $5 for a pill that costs 75 cents… and the pharmacy doesn’t even get the extra $1.25? It goes to some corporate suit in Connecticut who’s on a yacht right now? 🥴 I’m not mad… I’m just disappointed. And honestly? Kinda sick.

Lynn Steiner

December 8, 2025 AT 19:46My dad’s pharmacy closed last year. He worked 70 hours a week. Paid $180k in rent. Got reimbursed $3.50 for a $0.60 generic. They told him to "just sell more vitamins." Like that’s going to cover his payroll. America is broken. And we let it happen.